I’ve noticed that the older my kids get, the further away my marker gets for true adulthood.

When I was the mother of toddlers, older kids in high school and college seemed so grown up to me, ready to support themselves and make smart decisions. I’d see them driving around town, getting their first jobs, heading off to college, starting a career. Adults, right?

But then your own kids start to get to that age and you learn that despite this outward appearance of “young adulthood”, they are still just KIDS. Sure, they are getting there, but they won’t truly arrive for years to come.

In most states, they legally become adults at 18. As any parent of a 17 year old knows, that’s crazy talk.

The idea of not being “here” to get them all the way “there” is not a thought we like to ponder.

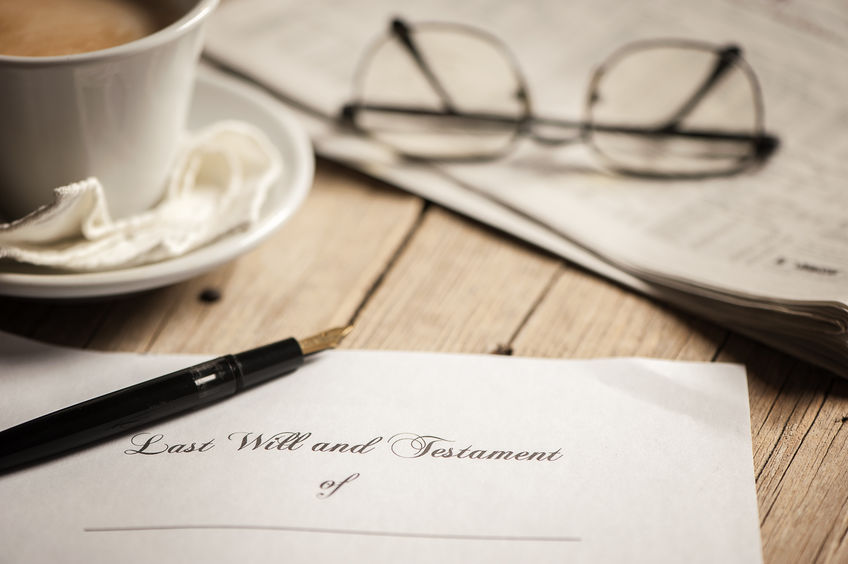

One of the things you can do as a parent is put an effective estate plan in place in the event something should happen.

This is even more critical if you are a single parent, as you are the last line of defense. Even if there is an ex-spouse involved in their lives, once the horse has left the gate (i.e. they inherit all of your assets outright), that parent has no legal say about how those assets are spent.

I shared last month that my husband and I were in the process of updating our estate documents. When we last updated them, age 25 seemed fairly adult to me, an appropriate time for our children to receive our assets should something happen to us.

Wait, what??? No way. I’ve changed my mind. At least not all of it, at once, for any old thing they wanted.

Pay off college loans? Sure. Buy a (reasonable) car? That makes sense. Maybe take a chance of a lifetime trip around the world before they start their career? Well, maybe.

Depending on what is going on in my kids’ lives at that time, I’ve legally entrusted their Auntie Beth to guide them in making good decisions around money while they continue to learn to make those sound decisions on their own.

When I meet with prospects and clients, I tell them that a financial plan is a living, breathing thing. It’s not just one and done. Life is always changing.

Estate planning, as part of your overall financial plan, is very much the same. You first create an estate plan when you are newly married or have young children. You can’t possibly create a single document that addresses all situations forever. You have no idea what life will look like in 5 years, never mind 25.

In addition, estate tax laws are ALWAYS changing and with that, estate planning techniques are adjusted to meet your needs within the context of these changes.

Life happens. If you haven’t updated your estate documents in the last 3-5 years, take time to review them now and answer these questions:

- If the proverbial “hit by a bus tomorrow” happens to you, is your estate in proper order for the person you trust with your life to step in, literally that day, and take over with as little roadblock as possible?

- Does this plan still reflect your wishes and the wishes you have for your beneficiaries?

- Are the people you’ve named as health care proxy, power of attorney and/or trustee still the ones you trust the most to handle these responsibilities? Are they getting older and maybe no longer the best choice? Are their values similar to yours? Remember, they may be making major decisions in your place.

- If you’ve created trusts, are your assets titled appropriately to “fund” the trust?

- IRA, 401(k) and life insurance assets pass by way of beneficiary designation and NOT by will or trust. Do you have beneficiaries named appropriately? Again, it does not matter who or what you have in a will or trust. It won’t apply to these types of assets.

Honestly, there are many other pieces of the estate planning puzzle to consider. A qualified estate planning attorney will walk you through it all.

You can’t take away the heartache, but you can alleviate some of the headache.

Financial Fitness Tip

Last March, I reminded you that you have until the current tax filing deadline to make IRA contributions for LAST YEAR.

But my tip this month is to point out that your child who works a part-time job can also still make a 2020 contribution – and it should be to a Roth IRA.

If they had earned income in 2020, consider opening a Roth IRA and having them fund it with their earnings or, if you are in a financial position to do so, fund it for them, or a combination of both.

They can contribute up to the lesser of $6,000 or their earned income for 2020.

They are most likely earning too little to owe any federal or state income taxes, which means this “income tax free” money is being invested into an account that will grow tax free forever. NO TAXES EVER, even when they take it out.

Of course, as with all qualified accounts, there are rules as to when distributions can be taken tax and penalty free, but as long as they follow the rules, this savings vehicle is a slam dunk.

My Favorite Quotes

I’m sure many of the women being honored this March for Women’s History Month followed this type of mindset:

“You can never leave footprints that last if you are always walking on tiptoe” – Leymah Gbowee