A friend recently came to me with a business idea that she felt could be really useful to many.

She felt quite strongly about it because she knew it would be very useful to HER, and she correctly assumed that many (many) others are in the same position.

Let’s call it:

I PAY LITTLE TO NO ATTENTION TO WHERE MY MONEY IS ACTUALLY GOING, and I could really use some help trimming the fat.

Her request was not so much about budgeting, but simply about TUNING IN, knowing where the dollars are going and trying to cut out the fat.

And let’s face it, with inflation having snuck up on us with a vengeance this year, we all need to covet and stretch every dollar, because our dollar can no longer afford what it could just 8 months ago.

Sometimes money “lost” is simply due to our failure to tune into things, like is that medical bill accurate, did you actually get the sales price advertised or are you sitting on unreturned merchandise.

I recently received a medical bill for almost $3,500. It looked right. I mean, we did use that provider on that date, and we do have a high deductible plan. BUT, because I tune into the EOBs (explanation of benefits) that come from our insurance provider, I knew our portion was only supposed to be about $1,500.

I potentially could have tossed $1,500 out the window if I had just paid it without tuning in.

I’m also a grocery store Ninja, I’ll admit it, even pre inflationary times. I should be on THE PRICE IS RIGHT.

And never more than now do I play their game because with three teenage football players in my house, you would not believe my grocery bill.

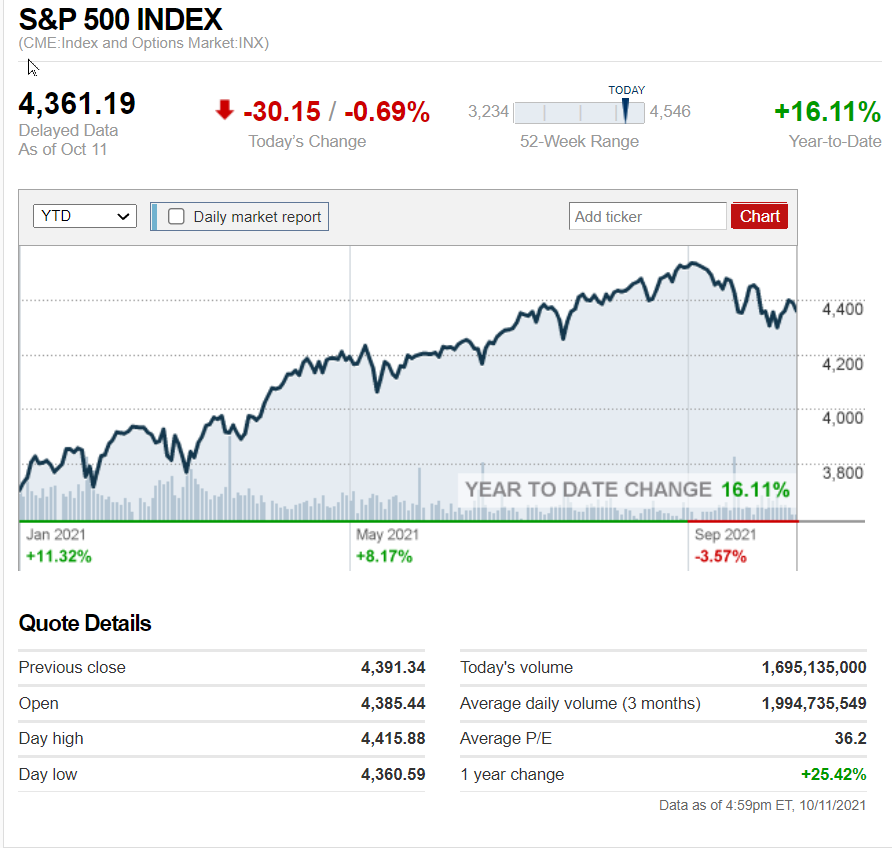

So while investing is an important aspect of your financial health, and it is disconcerting when the markets are down, it’s the day to day spending that you have the most control over that can make tangible differences.

If you feel like your spending could use some trimming (mine definitely could) and especially if you are finding you need every dollar just to cover the basics, here are some “tuning in” tips to think about:

Shopping:

- Get rid of Door Dash. I will not let my kids order anything on my dime through Door Dash. I never have. What a money suck that is! Old fashioned pizza delivery, sure, but not Door Dash. I saw a receipt once that showed my son paid $9+ to have an $11 burrito delivered!

- Tune into shipping costs and try to avoid. They can really add up.

- Shop the grocery store circulars. Use the apps if you need to for certain “big” deals. Stick to what you would normally buy, don’t buy it because it’s on sale. But if it’s on sale AND it’s on your list for the week-fantastic. Check the receipt before you walk out the door to be sure you received the sale price. Head straight to customer service if you did not.

- Buy store brand/generic wherever it truly does not matter, which is most of the time. But hey, we all have our favorites. I won’t give up my Charmin.

- Buy cards at The Dollar Store. Honestly, you should never again purchase a card anywhere else. They have great ones. And let’s face it, your money literally gets thrown in the trash after it’s opened!

- Return items you bought but will not be using. I’m a nut about returns. We all buy things either in store or on line that don’t work out as we had hoped, but you MUST return it or you are just throwing your money away.

- If you are a Target shopper, use the app to place your order ahead of time and have it delivered to your car. My personal experience is you end up spending much less when you are not walking the aisles. And unlike some of the on line grocery delivery services, there are no extra fees (yet).

I wish I could say “get rid of Amazon” but I’m trying to be realistic. 😊

Other:

- Employer benefits I’ve seen not insignificant amounts of money left on the table when people have not used plan benefits to their best advantage.

- Pay attention to bills you are receiving, even if you have them set to autopay. And medical bills for sure.

- Don’t carry a balance on your credit card. For every dollar you save with smart shopping, you’ll be paying way more in interest rate charges.

- Ask yourself the age old question, “do I need this or do I want this”?

Whatever your financial situation, remember the mantra to pay yourself first (savings) and spend less than you make. You’ll be on your way to sound financial footing!

Quote

Do not LET what you cannot do interfere WITH what you can do.

– John Wooden